No Recession in the Global Economy, but Divergence Aplenty

Yours truly is actually a macroeconomist, indeed with a knack for financial markets, but still; a macroeconomist nonetheless. However, you would not have gotten that impression from the writings here end last week where I worried a lot about the worry of financial markets. I still do, worry that is, mostly because we are in a very delicate situation where a severe shock in financial markets can easily and quickly be transmitted into the real economy. Moreover and as Edward eloquently conveys in his recent post the structural challenges we face are complex and difficult.

Yet, in terms of the immediate evolution in the real economy, and in case you had not noticed, the recovery is coming along just fine.

(click on pictures for better viewing)

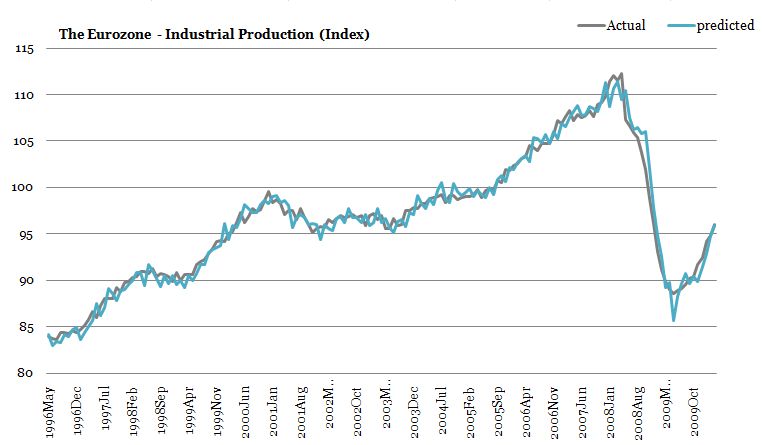

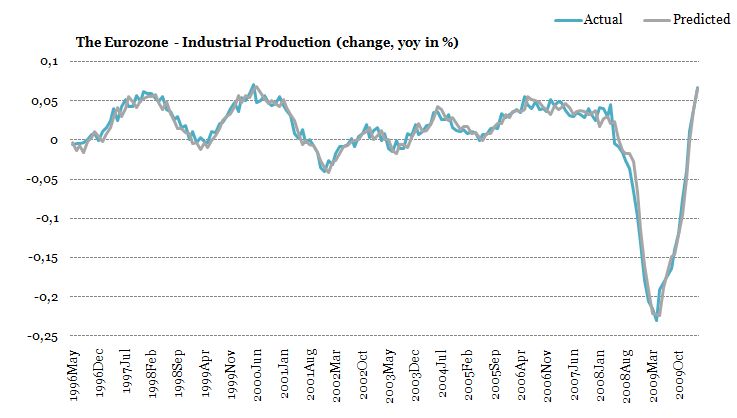

If ever there was a clearer sign of a v-shaped recovery I'd like to see it. On an annual basis the EMU industrial production index rose 11.6% in Q1 2010 and on the quarter the increase was 4%. Despite the emerging crisis in the Eurozone and with reservations for the final number of Q2-10, this suggests that the turnaround is intact so far. Naturally, the level of industrial production is still very low compared to before the crisis and, as I have argued, this is an important gauge in terms of the overall strength of the momentum. But, the recovery remains real at this point

Of course, it is not difficult to pick the positive discourse apart and this applies especially to the Eurozone there is a bound to be notable divergence between the growth rate of economies. In particular, it does not take much Roubinesque imagination to see what awaits the famed Eurozone periphery (Spain, Portugal and Greece) who are now about to embark on a very brutal spell of internal devaluation; kind of like in the Baltics who are undergoing the same [1].

This comparison may of course be inappropriate for a number of reasons, but it provides a good yardstick with which to look ahead into especially 2011 where the first part of austerity measures will really start to bite. Whether the Eurozone "core" remains enough momentum to pull the Eurozone forward is really not the important issue here. The real problem here is that from here on imbalances (not just external) will compound. In the lingo of development economics the convergence which was thought inevitable and on track is now about to unravel. In this respect, the comparison with key parts of Eastern Europe is well chosen I think.

And not just Europe...

Yet, if the outlook for Europe is still very uncertain the global outlook is positive for the remainder of 2010 even if the momentum appears to be flattening out;

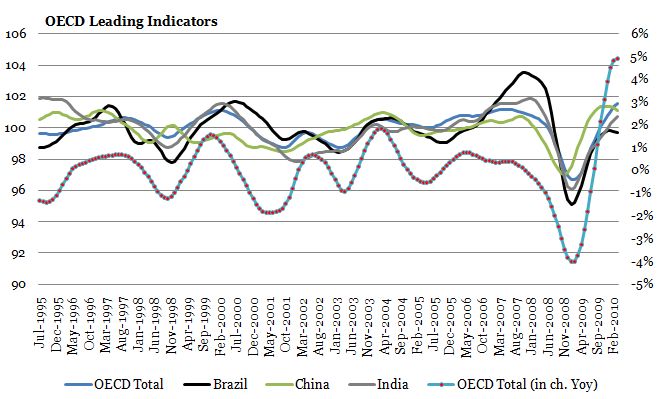

On an annual basis leading indicators for the major emerging economies as well as the OECD are coming in very strongly for Q1-10 and also over the quarter (i.e. from Q4-10) do we observe growth with the notable exception of China where activity seems to levelling off a tad going into 2010 on the back of continuing measures by the government to restrain the economy.

It is difficult to deny that the leading indicators tracked by the OECD seems to be flattening moving into Q2-10 and it will naturally be interesting to see whether momentum will be sustained. As ever, divergence both in levels and actual growth rates will be paramount to factor in, but I am very confident that we are not going to see a double dip recession in for example the US let alone the emerging market edifice in 2010. In Europe, the tug-of-war will between growth in France and Germany (with the latter exporting to EMs as the only real source of growth) and a continuing slump in Southern Europe. However, since 2010 budgets are already passed to indicate very stimulative policies throughout Europe the growth momentum will be strong in 2010 although the medium to long term look decidedly awful.

Event Risk still High

As a natural finishing point it should not escape market participants and analysts alike that event risk is currently at a very high level. In many ways, we already have an event in so far as goes the crisis in Europe but I can think of plenty of more sources of potential market destabilisers. The point here is then that at the current juncture the transmission between market distress and the real economy is likely to be strong and relatively quick. In this sense, the recent news that the interbank market is freezing over once again is indicative that not all is well and I am watching this very closely.

As such I maintain my somewhat bearish inclination and deep skepticism for where aggregate demand is actually going to come from in the medium to long term; this especially the case in Europe whereas I am much more constructive on emerging economies who are, for all intent and purposes, doing well (indeed almost too well in some cases).

A number of well known proverbs spring to mind here; is the glass half full or half empty? Is this the end of the beginning or the beginning of the end? Whatever methaphor you prefer forward looking indicators point to strong growth in the first half of 2010 (at least). The key message on the real economy will thus be one of divergence and especially how some economies are doomed to deflation and negative growth in nominal GDP (in the context of internal devaluation) while others will fly on the back of excess global liquidity. For me, this is the main meta-discourse currently describing the global economy.

---

[1] - Q1-10 GDP is only available for Lithuania so for the two others the calculations ends with Q4-09.